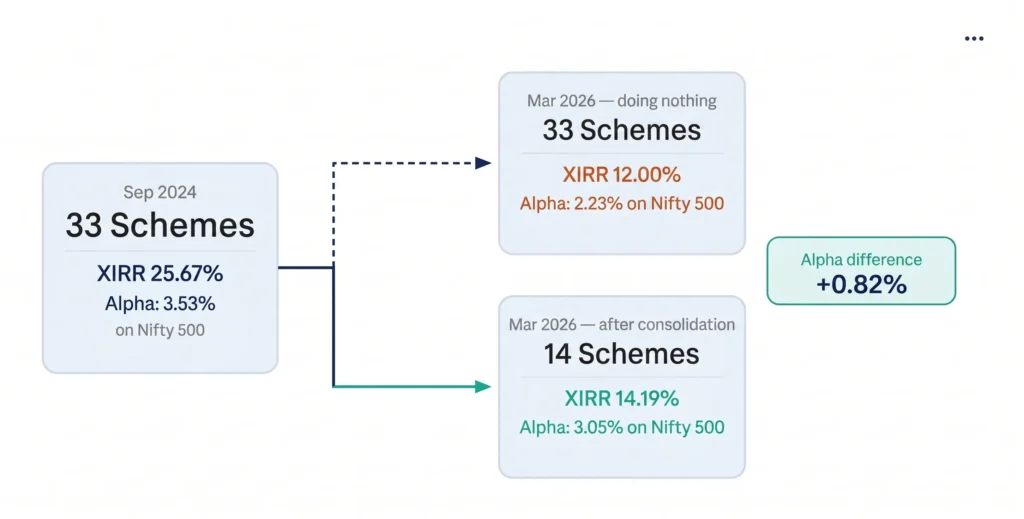

33 equity schemes. XIRR of 25.67% vs Nifty 500 at 22.14%. Alpha of 3.53%.

That’s how my portfolio looked in September 2024.

And 33 schemes was not an accident. It was a hypothesis.

The (weak) hypothesis

In 2021, I sat down and tried to think honestly about what I actually knew.

All the data available – rolling returns, Sharpe ratio, alpha, beta – is backward looking. My performance lies in the future. And there are 500+ equity schemes out there. The idea that anyone can pick 10 schemes and have all 10 outperform the index is, statistically, unlikely.

So I built a workaround.

What if I picked 3-4 schemes from each category – large-cap, mid-cap, small-cap, contra, focused – kept allocation to each one low, around 4-5%, and simply observed? Let them run. See which ones emerged as consistent winners. Then cut the losers and concentrate into what was working.

The logic was: I can’t lose meaningfully on any single scheme at 4-5% allocation, and over time the winners and losers will separate themselves.

Sounds like a well-thought out logic. But only later would I know that I was missing out on one of the most important things: the current market cycle.

But I didn’t know it back then and that’s how I reached 33 schemes by September 2024.

It worked. Until it didn’t.

The thing that I ignored – the bull market cycle – was noticeable when it ended.

The bull run paused, then reversed. And the losers started emerging – except it wasn’t one or two schemes lagging. It was the entire portfolio moving together. When I tried to decide which schemes to keep and which to exit, I had nothing to stand on. No principles beyond performance. And performance, in a downturn, tells you nothing useful about what to do next.

Should I sell the underperformers? Should I sell everything in that category? Should I hold and wait for mean reversion? Should I add more at lower NAVs?

I had 33 schemes and I couldn’t answer any of it.

So much for a well-thought out strategy.

What did I observe & change?

The problem wasn’t the number. The problem was that my hypothesis – observe, identify winners, cut losers – had assumed that past relative performance would tell me which managers were genuinely better. It doesn’t. In a bull run, most active managers look good. The market was doing the work, not them.

So I had to build a different framework. One that looked beyond performance.

The principle I arrived at: develop your own view on macro, sectors, and earnings. Find fund managers whose positioning reflects that view. Allocate substantially to them. But also allocate to one or two managers who hold a different view — because you might be wrong.

This changed everything about how I looked at my 33 schemes. The question was no longer which scheme has the best 3-year rolling return. It became: which fund manager’s reading of the market do I actually believe – and am I holding their scheme in any meaningful size?

Most of my 33 schemes failed that question immediately. I had schemes I held at 4-5% allocation with no real conviction behind them.

I cut to 14 schemes. Here’s what happened to the numbers.

March 2026: XIRR 14.19% vs Nifty 500 at 11.14%. Alpha: 3.05%.

The alpha had dropped from 3.53% to 3.05%. For a moment, that looked like a mistake.

So I ran the reverse experiment – what if I had done nothing & held all 33 schemes through to today?

Results would be – XIRR: 12.00%. Nifty 500: 9.77%. Alpha: 2.23%.

The portfolio I consolidated is delivering 3.05% alpha. The portfolio I would have kept at 33 schemes would be delivering 2.23% alpha. It tells me that the losers were real losers – it wasn’t just a fluke. And that the winners were worth holding on to.

My Lessons

Two things this taught me that I don’t hear enough:

In a bull market, everything works. Scheme count, fund manager quality, category selection – none of it is truly tested when the tide is rising. The test comes when it turns.

And there is no ideal number of schemes. Everyone will tell you “12 schemes? That’s too many.” No statistical evidence behind that claim – only rhetorical warnings about overlap and over-diversification. The number is not the point.

The point is whether you or your advisor have a view.

Not a view on which scheme has the best Sharpe ratio. A view on what the market is doing – which sectors have earnings momentum, which are overpriced, where the macro is heading – and whether the fund managers you’re paying to allocate your money share that view or productively challenge it.

If you can answer that, 14 schemes is fine. So is 20.

If you can’t, 6 schemes is just as random as 33.

About Prathamesh

I am an IIM Bangalore alumnus. I was wealth manager for some of the riches HNI-UHNI families in India. Then I decided to venture out on my own to bring that expertise for everyday Indians. I am working to make highest-grade investment advisory accessible to every Indian. IMO the lesser the welath someone has, the more they can benefit from professional guidance. I like to write and talk about everything finace - investing, insurance, debt management, behavioral finance and so on. When I am not writing, I am making educational videos. And when I am not doing that either, I am catching up with the lates comedy or thriller shows and movies.