A debt fund giving 12–13% annualised returns, especially in a year when equities have been rough. That sounds like the obvious move – equity like returns with safety of bonds.

That reasoning is exactly the trap.

Two credit risk funds have been doing rounds on Reddit threads and Instagram reels lately: Aditya Birla Sun Life Credit Risk Fund and HSBC Credit Risk Fund. The numbers look like this:

Those are debt fund returns. You read them right. And they’re enticing precisely because they’re misleading.

What credit risk funds actually do

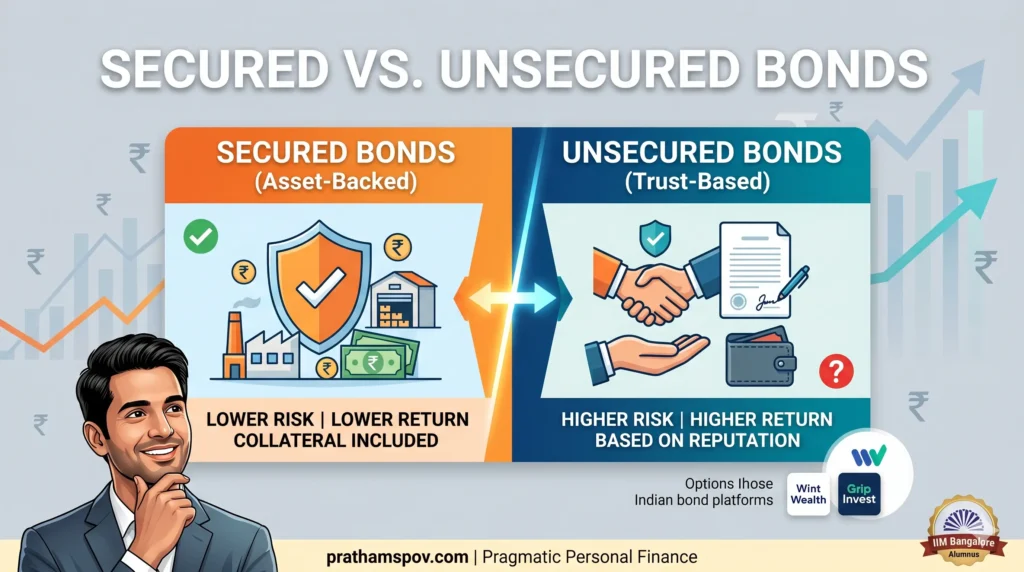

Most debt funds lend to companies with high credit ratings – think government bonds, AAA-rated paper. A credit risk fund does the opposite. It deliberately lends to companies with lower credit ratings in exchange for higher interest (sometimes unsecured bonds). Think of it as the difference between lending money to a salaried government employee versus lending to your neighbour who runs an unpredictable business. The neighbour pays you more interest — but you’re taking a real chance he defaults.

These two funds took that chance. And a few years ago, it went wrong.

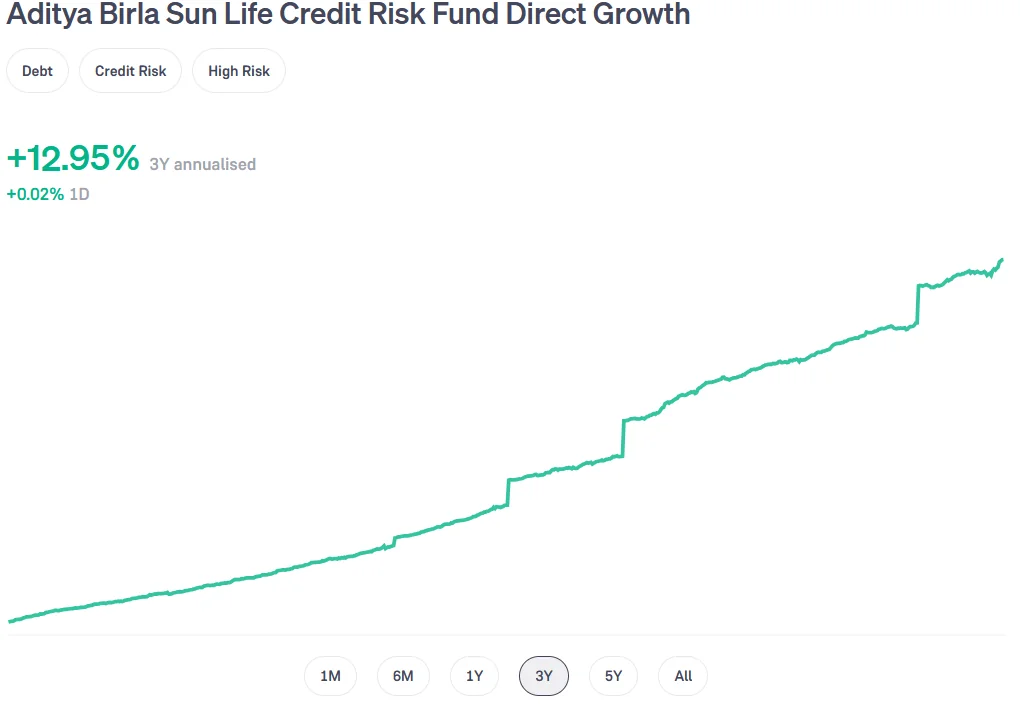

The past that’s now flattering the present

ABSL Credit Risk Fund had invested in 11 lower-rated bonds that went bad. The fund wrote those bonds down — meaning they marked their value at 0 to 50 paise on the rupee in the NAV calculation. If the fund had invested ₹100 in a bond, it was valuing that bond at ₹0–₹50 when calculating what your units were worth.

Think of it like this: you lent ₹1 lakh to someone, and after two years of missed payments, your accountant tells you to record that loan at ₹40,000 in your books. You still hope to recover it. But right now, officially, you’ve taken a write-down.

HSBC’s fund had similar write-downs, concentrated in fewer bonds.

When a written-down bond starts paying back — through asset sales, legal recovery, or restructuring — the NAV doesn’t slowly climb. It just jumps. That spike isn’t earnings. It’s a reversal of a previously recorded loss.

The NAV charts of both funds tell this story clearly. ABSL has multiple small bumps — many bad bonds, multiple partial recoveries. HSBC has one dramatic vertical spike — fewer bonds, one large recovery.

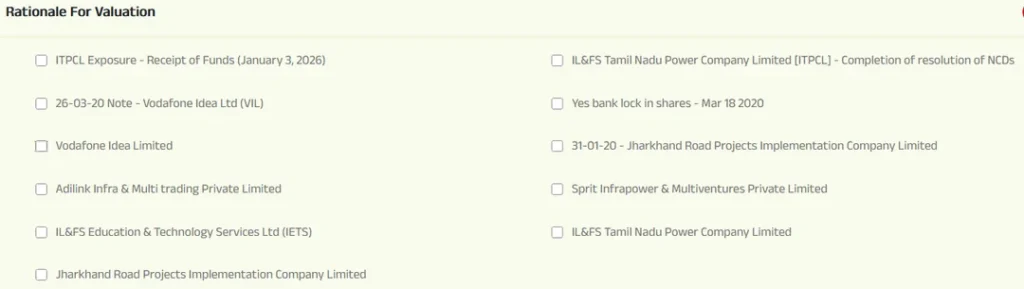

The spikes you see in those charts

January 2026 — ABSL Credit Risk Fund: Received ₹36 crore from IL&FS Tamil Nadu Power Company Limited. NAV jumped 3.32% in a single day.

April 2025 — HSBC Credit Risk Fund: Recovered ₹66.4 crore against bonds of Reliance Broadcast Network Limited. NAV moved +11% in a single day.

Those recoveries were not guaranteed. There was genuine uncertainty about whether this money would come back at all. If those payments hadn’t happened – or if they’d come at a fraction of the amount- both funds would look like the worst performers in the credit risk category. Which, if you strip out the recoveries, is exactly where they’d rank.

Who actually made money here — and who funded it?

The investors who were in these funds in 2018–2019 are the ones who absorbed the original loss. They watched their NAV stagnate or fall while the bad bonds sat on the books. Many of them sold – frustrated, or needing the money. When the recoveries came, they weren’t around to benefit.

The people who invested after the write-downs – when the NAV was already depressed – got rewarded when the recovery hits landed.

This is what the returns are actually measuring: not the fund manager’s skill, not a reliable strategy — but the timing of when you happened to buy relative to when a contingent legal recovery happened to arrive.

If you invest now, you don’t know which position you’re in. You could be the 2018–2019 investor, sitting through the next cycle of write-downs. The recoveries these funds are celebrating now are already in the NAV. There may not be another spike coming.

Why this matters specifically for your emergency fund?

Emergency funds have one job: be there when you need them. Not generate returns. Not beat FDs.

If your emergency fund is parked in a fund that can see its NAV drop 10–15% on a bad credit event, and you lose your job the same week — you’re withdrawing at a loss. That’s the worst possible version of this: the emergency and the loss arriving at the same time.

Earn a little less. Use a liquid fund or a short-duration fund for your emergency corpus. The 2–3% you might “give up” is insurance, not waste.

One more thing about those star ratings

I checked how major platforms are rating these funds. Both are sitting at 3–4 stars.

Platforms claim their ratings factor in risk-adjusted performance. But when a fund that had a near-complete write-down of 11 bonds gets 4 stars because its recent 1-year return looks good — that tells you something. Past returns still carry very heavy weight in how these ratings are calculated, regardless of how the returns were generated.

A star rating tells you what happened. It does not tell you why. Understanding the why is your job – and this is what it looks like in practice.

P.S. Credit risk funds aren’t inherently bad. Some investors deliberately use them as part of a diversified debt portfolio, with full awareness of the risk. The point here is narrower: don’t use them for money you cannot afford to have frozen or reduced at short notice.

About Prathamesh

I am an IIM Bangalore alumnus. I was wealth manager for some of the riches HNI-UHNI families in India. Then I decided to venture out on my own to bring that expertise for everyday Indians. I am working to make highest-grade investment advisory accessible to every Indian. IMO the lesser the welath someone has, the more they can benefit from professional guidance. I like to write and talk about everything finace - investing, insurance, debt management, behavioral finance and so on. When I am not writing, I am making educational videos. And when I am not doing that either, I am catching up with the lates comedy or thriller shows and movies.