If you don’t have some basic idea about what bonds are then you can check out this article where I have explained what a bond is and how it is created in the simplest terms possible.

And if you already know the basics about bonds, read on.

2 Types of Loans

Secured Loans

Banks offer various kinds of loans to people and companies. All of those loans can be divided into just two categories – secured and unsecured.

A secured loan means that the person or the company that took the loan (called borrower) has given an asset as a collateral to the bank (called lender). This means that if the borrower fails to pay the EMIs, then the lender can take control of that asset, sell it, and recover their money with interest. Home loan is the best example of a secured loan. It is often called “asset-backed” loan. And because the loan is backed by an asset, the lender gets some guarantee that they will be able to recover their money. That’s why the interest rate on secured loans is usually lower.

Unsecured Loans

On the other hand, in case of an unsecured loan, there is no asset given as collateral by the borrower. So, what if the borrower doesn’t pay? Then since the lender can’t claim any assets, they have to recover it in other ways like giving it to loan collection agencies, sending legal notices, or offering to settle for a lower amount. In some cases where the loan amount is huge, the lenders may file a court case on the borrower, and get a legal order to sell their other assets to recover as much money as possible. This process of recovery might take months or years to finish. And recovery most often happens only for 40-60% of the amount. And that’s why, as you would have already guessed, the interest rates on unsecured loans are higher by 2-4% compared to secured or asset-backed loans. Personal loans are an example of unsecured loans.

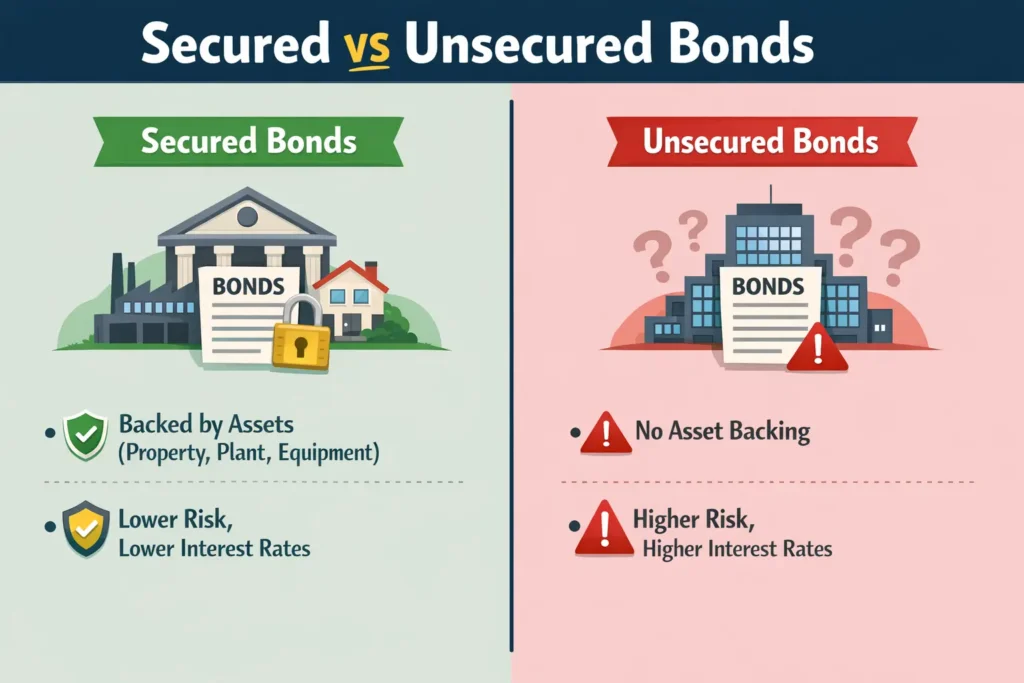

2 Types of Bonds

Now since bonds are essentially loans that the company takes from the bond-buyers, the two types of bonds are secured or asset-backed bonds, and unsecured bonds. The company who takes the loan by selling the bonds becomes the borrower, and the ones buying the bonds (people like you and me, or other companies) become the lenders. The company may decide to make the bonds – which is a loan – either secured or unsecured, depending on its size, reputation in the market, and the economic conditions.

Secured Bonds

When the bonds are secured, the company assigns specific assets like its plant, building, machinery, the money receivable from its customers as collateral. If the company for some reason doesn’t pay either the coupon or principal to the bondholders, then they can claim those assets, sell those, and recover the money they were supposed to receive as principal and interest. In most of the cases, such recovery doesn’t always get you your full money back. For example, if you had invested Rs 100, you might be able to recover anywhere between Rs 0 (if the assets have become worthless for some reason, rare scenario) and Rs 100 (best case scenario). And because of this freedom that bond buyers have, the interest rate on secured bonds is usually lower compared to unsecured bonds.

Unsecured Bonds

You might have already concluded what unsecured bonds are. There are no assets backing those bonds. Which means, if the company doesn’t pay you interest and principal for some reason, you can’t really sell their assets. In most cases, the money is gone. Then why do people buy those? Because of the reputation of the company issuing the bonds. And that’s why you will see that only bigger and reputed companies like State Bank of India, Tata Motors, Reliance Industries etc. can issue such unsecured bonds and also find buyers willing to take those bonds and the risk that goes with them.

The inverse is also true. That is if a company is not very big, they have to focus on issuing secured bonds (asset-backed bonds). If they don’t do it, they might not find any buyers and hence, won’t be able to raise money. And if they do manage to find some buyers, those buyers will ask for interest rates (coupon) way higher than unsecured bonds of bigger companies. For example, if SBI can find buyers by offering 8% coupon for its unsecured bonds, a small company might have to offer 10-20% coupon to find any buyers, depending on the rating given by the rating agencies.

Conclusion

Most investors buy bonds in order to add stability to their overall portfolio. They are less volatile than equity, and generate returns higher than most fixed deposits out there. In India, bonds are available to buy on platform like Wint Wealth, Grip Invest, India Bonds and so on. They have both secured and unsecured bonds. And like I said, if you want to invest in bonds of smaller companies, always prioritize investing in secured bonds. Also, it will be less stressful to buy bonds which have smaller maturities like a few months to 1 year. Because as the maturity increases, the uncertainty that something will go wrong with smaller companies increases, eventually resulting in loss of your entire or some part of the invested amount.

You also now understand why bonds offer higher returns than fixed deposits. The online platforms promote fixed and guaranteed returns of 9-14% from bonds but in returns for those extra returns, you give up a few things. The first is peace of mind. You never know what can go wrong with a company. Equities in most cases decline gradually. But when something goes wrong with a bond, it happens in a single shot and you don’t get much time to exit. Secondly, you can withdraw your money from fixed deposits any time. If you want to sell bonds, you need to go out on exchanges like BSE and NSE and hope there is someone who is willing to buy the bond you are selling. Even if you find a buyer, you will have to sell it at a lower price, depending on how badly you need the money.

We will get into the details of risks of bonds in a separate article. But knowing this much, I think bonds are not suitable for most of the retail investors. The portfolios are generally in the range of few lakhs, and if someone puts Rs 25,000 in bonds and loses that money, it’s not a small loss in percentage terms. The good old boring fixed deposits and debt funds are much better options.

So that’s my point of view. Do you agree? Let me know in the comments.

Thanks for reading,

Prathamesh

If you’d like to receive updates about my next post on email, Click Here.

If you’d like to receive updates about my next post on WhatsApp, Click Here.

By signing up, you agree to the Terms and Conditions and Privacy Policy of our website.

About Prathamesh

I am an IIM Bangalore alumnus. I was wealth manager for some of the riches HNI-UHNI families in India. Then I decided to venture out on my own to bring that expertise for everyday Indians. I am working to make highest-grade investment advisory accessible to every Indian. IMO the lesser the welath someone has, the more they can benefit from professional guidance. I like to write and talk about everything finace - investing, insurance, debt management, behavioral finance and so on. When I am not writing, I am making educational videos. And when I am not doing that either, I am catching up with the lates comedy or thriller shows and movies.