You might have seen ads of bonds everywhere these days, getting you curious to ask what a bond is. The ads throw words at you like “Safe”, “Guaranteed”, “Fixed”, “Passive Income” when they talk about bonds. So let’s understand what a bond is and is a bond really all that the ads say that they are.

What is a bond?

A bond is simply a “loan”. Think about what happens when you take a loan from a bank, like a home loan. First of all, you decide that you want to buy a home which costs Rs 50 lakh. Since you don’t have the entire money, you approach a bank for the loan. When you visit the bank, the first thing the bank does is check your credit score and your loan history – how many loans you have, do you pay your EMIs regularly, how much is your income and so on. These things matter to the bank because they don’t want to give money to someone who will not repay them with interest. They will lose money if they gave a loan to anyone without checking these things first. That’s why they are extremely careful before they decide to give a loan.

Only after you pass these checks they decide to give you a loan. Once that loan is approved and the loan amount hits your bank (or the builder’s account), you have entered into an agreement with the bank. You have promised them that you will repay it with interest through monthly EMIs for the next 20 years.

It works the same way when you buy a bond of a private company. It is an agreement between you and the company – you will give them a certain amount as a loan, and they will pay you interest on that amount. The only difference between a bank loan and a bond is that bonds can be transferred from one person to another. That is to say, bonds can be traded. Let us now understand how bonds are created.

How are bonds created?

Suppose a company decides to build a new plant because the demand for its product is going up. Building a new plant will cost them Rs 200 Crore. But there’s one problem – they don’t have the money. So they decide to take a loan and approach a bank. And the bank does the same thing with the company they did with you – analysing their income & expenses, their existing loans, and how honestly they repay those loans. After all this analysis, suppose the bank decides to give the company a loan of Rs 100 Cr at an interest of 10% per year and the company must repay the loan in 5 years. Good news, but the company still needs Rs 100 Cr more. And when they go out looking for someone who will lend them the money, they find that no single person wants to give them a loan of Rs 100 Cr. So what can the company do? The answer is creating bonds.

The company on seeing that no single person will give them Rs 100 Cr, decides to divide the loan in 100 parts, with the value of each part being Rs 1 Cr. Each part that costs Rs 1 Cr is called a bond. It looks like 100 loans of Rs 1 Cr each from our point of view. From the company’s perspective, it’s a single loan divided into smaller parts. The company says they will pay the same interest of 10% per year, will make payments every month, and will return the principal after 5 years. Notice this that in case of bonds, you will get your investment amount back only at the time of maturity. Let’s understand some terms related to bond using this example.

Important Terms related to a bond

- Face Value or Par Value or Principal: This is the value of the single part of the loan. In our case, it is Rs 1 Crore since the company has divided a Rs 100 Cr loan into 100 parts. The interest is calculated on the basis of the face value. All these 3 terms mean the same thing.

- Coupon rate or Interest Rate: The rate of interest that the company will pay you is called coupon rate. In this case, coupon rate is 10% of the face value of Rs 1 Cr

- Coupon Amount (or simply, coupon): The interest amount that you receive from the company periodically. For example, if you buy one bond of Rs 1 Cr, your coupon amount will be Rs 10 lakh, which is nothing but face value multiplied by the coupon rate.

- Payment Frequency: The frequency at which the company decides to pay you. The company in our case will pay an interest of 10% per year totalling Rs 10 lakh, but it will pay it monthly. So every month, you will receive ~Rs 83.33 thousand.

- Maturity Date: The date on which the company will return your Rs 1 Cr principal after 5 years, along with the final coupon of ~Rs 83,000 for the last month.

I have avoided giving technical definitions here because IMO what matters to you as an investor is not getting the technical definitions right, but understanding what those terms mean. Once that is done, we go to the next part – what are the risks in bonds?

Risks in Bonds

Think again about how much homework the banks do when you go to them for a loan. They check your credit score, your outstanding loans, your income, and how you pay your EMIs on time. Sometimes, if your credit score is extremely good, then you get your loan at a lower interest rate. If your score is average then you pay a slightly higher interest rate. And if your score is bad, then the banks don’t even give you loans in many cases.

So when you are buying a bond, you need to act like the bank and do your homework. You need to know how the company earns, how much it earns, how much it spends, whether it has too many loans already and so on. But individual investors can’t do all this study because they either lack the skills or the resources to do all this work. And that’s where credit rating agencies come into the picture.

Credit rating agencies like CRISIL, ICRA, CARE etc. do this homework on the companies and based on their analysis assign each company a rating. These agencies do the same job for companies which CIBIL does for us – evaluate whether this person should be given a loan? A rating is nothing but a credit score for the company. But instead of scores, they assign letters for the rating. Investors can use the rating of a company to understand how reliable the company is whose bond you are buying.

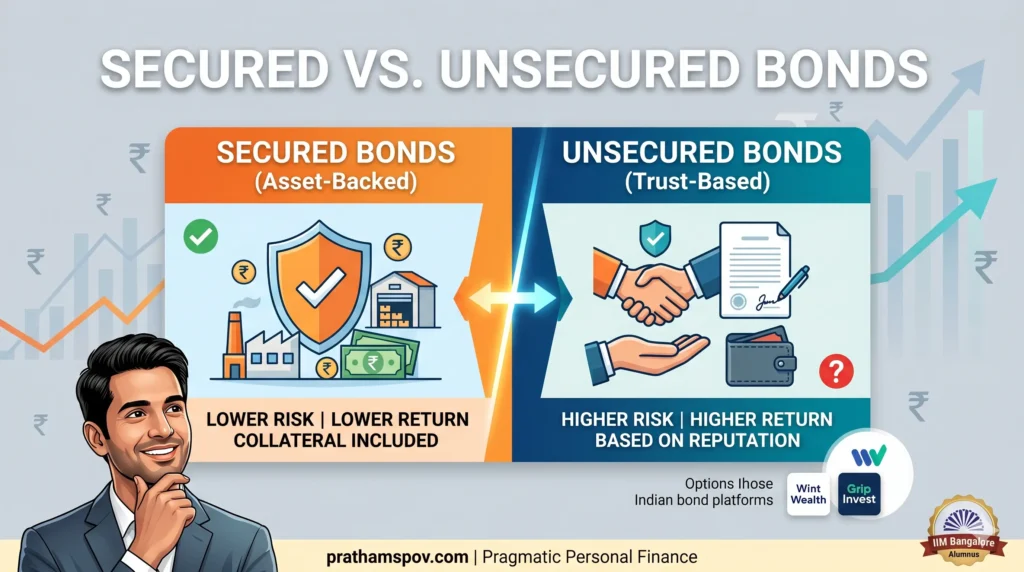

For example, when a bond has rating of AAA, it means that there is a very high chance that you will get your interest payments on time, as well as get back your principal at the time of maturity. The worst rating is usually D which is given to bonds of companies which are likely to not pay either interest or the principal to bond buyers.

And this is the biggest risk that you should know about as a beginner when you are buying a bond: whether the company will repay the money it took from you. In technical terms, this is called credit risk. And as I explained earlier, you can use ratings to understand how risky the bond of a company is when you are putting your money in it.

A word of caution though – a CIBIL score of 750 and above doesn’t guarantee that a person will repay 100% of the time. Anything can happen to a person when the loan is ongoing – he may lose his job, or his business may suffer or he may pass away. Similarly, just because rating is AAA does not mean a company will always pay no matter what. If the company’s business struggles and they can’t sell their product, even they may default, resulting in investors losing their money.

There is also a second risk. As I mentioned earlier, the bonds are tradable, i.e. you can sell your bonds to someone else when you need the money. However, in India it is not an easy thing to do. We have NSE and BSE for buying & selling of stocks with thousands of traders. But we don’t have such a huge platform where we can easily sell a bond, and the traders are usually only a few hundred for bonds rate below AAA. And even the AAA bonds trade in multiple of lakhs of rupees. So for a retail investor, selling a lower rated bond is not easy at all.This risk of not being able to sell your bond when you need the money is called liquidity risk. So credit risk and liquidity risk are the two most important risks for bonds in India.

Conclusion

So should you invest in bonds? Honestly, like all investment decisions, it depends on your goals and your unique needs. Do you need periodic income because you have no other source of income? Then bonds can be for you. Are you a highly conservative person who gets worried on seeing the value of his investments go down? Then bonds may be considered.

So bonds may be all those things we saw in the beginning, but as we saw later, there are risks as well. And the biggest risk is losing all of your money (credit risk). When a bond is offering you an interest higher than a bank Fixed Deposit, you have to understand that it is not the generosity of the company, but simply that bonds are riskier than fixed deposits.

Since this article was written for beginners, I didn’t go into many important details like yield-to-maturity, duration, modified duration, puttable bonds, callable bonds etc, in order to not overwhelm you.

See, when people watch the attractive ads about bonds on YouTube, Facebook, Instagram, in newspapers which promise you fixed, guaranteed returns of 10-12% , they get enticed and invest without fully understanding it. Sometimes it’s a friend who tells you that you should invest in bonds because he did. And in all likelihood, he or she has not done their homework either. Remember how much homework the banks – which have thousands of crore rupees – do when you need a simple loan of Rs 1 lakh. But people don’t do that much when they put their hard earned money in bonds. And most of those people don’t have thousands of crores of rupees with them. This article is for those people who are saying to themselves – “if bonds are so safe, why should I not invest in them? Am I stupid for not investing in them?”

I hope this article does a good enough job at helping you get basic answers about bonds and get some clarity on your decision making.

Still have doubts? Let me know in the comments.

Thank you for reading,

Prathamesh

If you’d like to receive updates about my next post on email, Click Here.

If you’d like to receive updates about my next post on WhatsApp, Click Here.

By signing up, you agree to the Terms and Conditions and Privacy Policy of our website.

About Prathamesh

I am an IIM Bangalore alumnus. I was wealth manager for some of the riches HNI-UHNI families in India. Then I decided to venture out on my own to bring that expertise for everyday Indians. I am working to make highest-grade investment advisory accessible to every Indian. IMO the lesser the welath someone has, the more they can benefit from professional guidance. I like to write and talk about everything finace - investing, insurance, debt management, behavioral finance and so on. When I am not writing, I am making educational videos. And when I am not doing that either, I am catching up with the lates comedy or thriller shows and movies.